Measuring success

Gilded Ages and what comes after.

“…the success of the republic is now measured by low prices and a high GDP.”

This quote, from a recent op-ed in the Economist, jumped out at me. The piece was written by Richard White, a professor of American History at Stanford, and compares our today with the American Gilded Age of the late 19th Century. As most Economist pieces are, it is brief and worth a read.

White calls the Gilded Age a transitory period. The hopeful “triumph of free labor” in the American Civil War brought with it “a conviction that the central purpose of the American economy was to sustain the republic. It should produce economically independent citizens who could not be dictated to or corrupted by the rich and powerful.” Instead, the Gilded Age produced:

“a different measure of economic success: the maximum production of wealth. Individualism, once identified with economic independence, became synonymous with the ability to acquire riches. Wealth became the measure of merit and ability. How it was distributed was not the concern of the republic.”

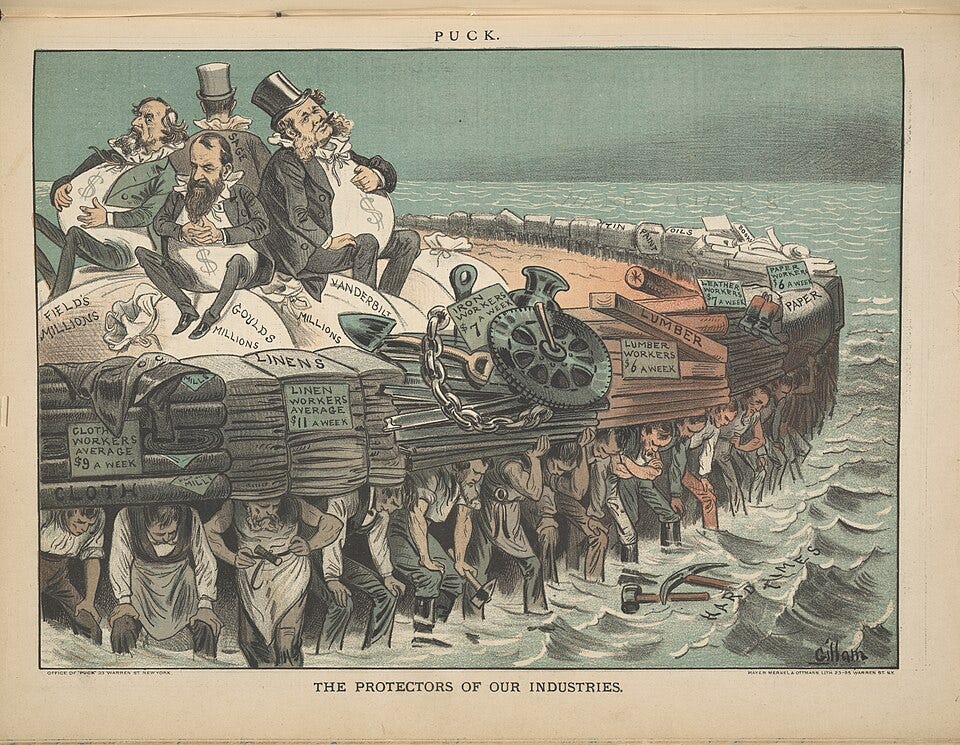

That wealth, “driven by the seizure of a continent rich in resources and the ample labour provided by mass immigration” and best articulated in the railroad industry, was concentrated in the hands of a few. The concentration of that wealth defined the politics of the age, which “became a battle between anti-monopolists and their opponents.”1

In describing our current times, White says that":

“America has not replicated the original Gilded Age. It has, however, created yet another version of hot-house capitalism that allows the worst traits of the Gilded Age to reappear. And it has added new ones: the 19th-century plutocracy never produced the strongman that the Founding Fathers feared would endanger the republic.”

White claims that our time is “missing…[the] modern equivalent of 19th-century anti-monopoly politics.” I’m not so sure. While he may be right that there is no substantial bipartisan coalition advocating “for an even playing field and a broad conception of public welfare,” there are strong anti-corporatist movements in both parties. On the left, they are relatively well defined and represented by DSA and Justice Democrats. On the right, the anti-elite threads are there but remain muddled in the gravitational pull of Trump and MAGA.

Which brings us back to the quote that headlines this post. It reads in full:

“Meanwhile, the belief that the economy should produce independent republican citizens has been flipped on its head; the success of the republic is now measured by low prices and a high GDP.”

I would hazard a guess that if you polled Americans, the vast majority do believe that the “economy should produce independent republican citizens”. That belief though, is undermined by the reality that is outlined in the following clause: that “the success of the republic is now measured by low prices and a high GDP.”

I want to break this down here concept by concept.

The “success of the republic” can be seen in a couple ways. First, the way that White likely means it, is the republican nature of our government. The Gilded Age was ripe with corruption and he cites the modern equivalent of the tech CEO’s “crowd[ing] the stage” at Trump’s second inauguration. This is plutocracy manifest.2 As White puts it, “Plutocrats, whose power threatens to corrupt the republic, are back. Wealth and political power once more seem inseparable. Self-dealing is commonplace.” Another related way to read this (like I initially did in light of my recent posts) is the “success of the republic” as the continuation of the social contract and the legitimacy of the state.

That legitimacy is now “being measured by low prices and a high GDP”. Low prices are an easy synonym for the defining word of the political moment: affordability. High GDP3, on the other hand, can be translated as economic growth.4

What happens if those two concepts, low prices/affordability and high GDP/growth, are zero-sum? That is, you can’t increase one without decreasing the other. And if they are zero-sum, and a state needs both to succeed, where does that leave us?

This brings us back to William I. Robinson’s work, which I first covered a few weeks ago, introducing his recent book Epochal Crisis and going through the multiple, self-reinforcing crises that define our era. I spent a paragraph or so on this idea of the contradictory mandate of the capitalist state that I find convincing and want to go more in depth into here.

For Robinson, The contradiction for the capitalist state is that it must “reproduce the capitalist relations of production within their nation-states, but they also must achieve a measure of consent among the working and popular classes…”

Let’s translate that.

The “capitalist relations of production” are essentially all the things that makes a capitalist economy capitalist. In other words, governments must create the conditions for capitalists to own the means of production, that is, those with money to invest that money. It must also create the conditions for the working classes to sell their labor to capitalists in a way that creates value for the capitalist.5 That they must do this in a globalized economy in which capital (again, read: money) can travel more or less anywhere puts further pressure on the state to “meet the needs of capitalists, for otherwise they will withdraw their capital from circulation and throw the economy into crisis.”6

That they must “achieve a measure of consent among the working and popular classes” is more straightforward and, I will yet again, just reference the social contract as the foundation of state legitimacy.

Between creating the “capitalist relations of production” and the “consent among the working and popular classes”, you essentially have White’s two conditions for the success of the republic.

A quick throwback to old school SAT prep for you just to clarify where I’m coming from here…

Capitalist relations of production : high GDP :: consent among working and popular classes : low prices.

Okay, so, per Robinson, capitalist states must strike a balance where it “can address enough of the demands of each to achieve broad legitimacy and stabilize the national social order.” Specifically this occurred in the “social democratic capitalism” that coincided with “high growth rates” in the “core capitalist countries in the post-WWII world.” That is, the world that Roosevelt’s New Deal and the subsequent neoliberal order built.7

I’m going to quote Robinson at length here because I think his point is important:

My concern is to focus on the contradiction between the need that the national state has to promote transnational capital accumulation in its territory in competition with other states and its need to achieve political legitimacy and stabilize the domestic social order. Attracting transnational corporate and financial investment requires providing capital with investment incentives such as low wages and labor discipline, a lax regulatory environment, tax concessions, investment subsidies, privatization and deregulation, and so on – the policies that have been pursued worldwide since the onset of globalization. The result is rising inequality, impoverishment, and insecurity for working and popular classes, precisely the conditions that throw states into crises of legitimacy, destabilize national political systems, and jeopardize elite control.

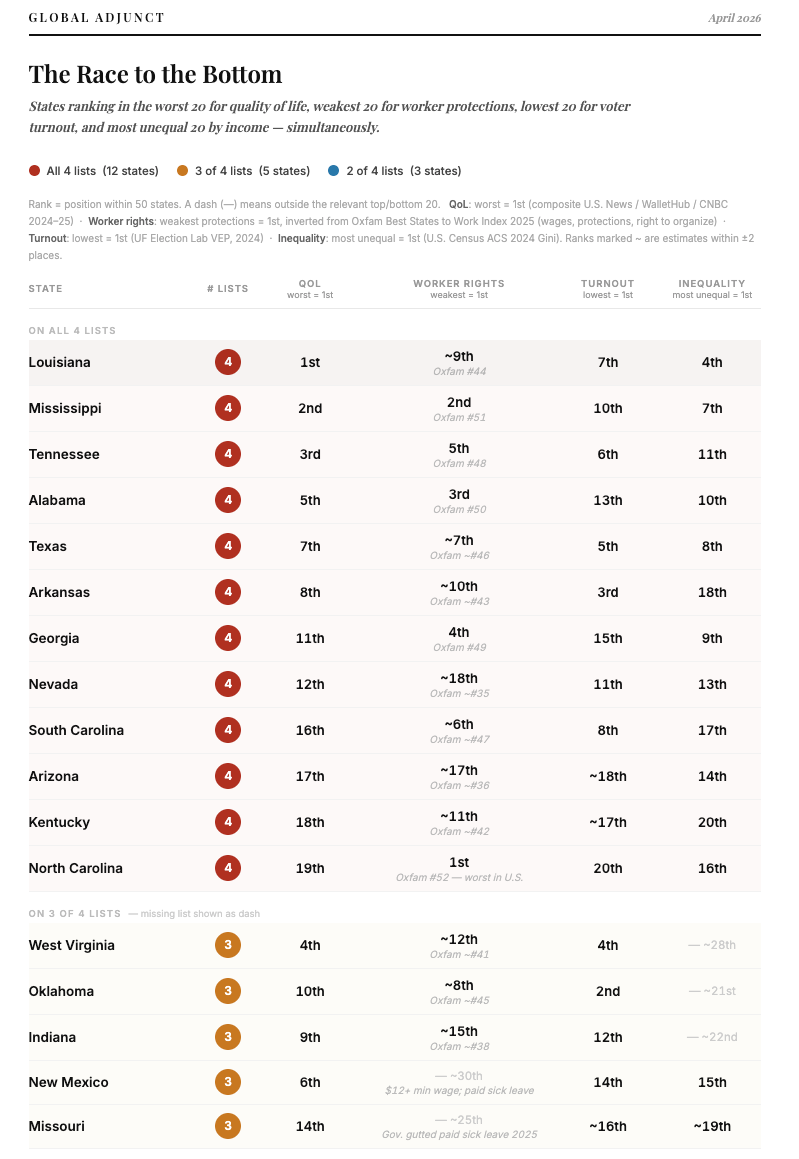

In fact, you don’t have to look internationally to see examples of what Robinson describes. Because American states are “laboratories of democracy” you can see these trends domestically as well. I had Claude compare the 20 states with the worst quality of life, the weakest workers’ rights (ie most friendly to capital), the lowest voter turnout (while imperfect, I’m using civic engagement as a measure of state legitimacy), and the highest inequality.8

The results, which I screenshotted below, are stark. 12 states were all four of the lists while another five were on three lists. These include Oklahoma and Indiana, both of whom are the 21st and 22nd most unequal, respectively, and Missouri who was 25th in workers’ rights and whose governor gutted paid sick leave in 2025.

The fact that Claude titled this chart “Race to the Bottom” is illustrative. Especially in times of economic hardship, state governments have competed to lure capital, nearly always at the expense of their social safety nets. The states that have “won” the race are on chart above.

White ends his piece with the following: “In the late 19th century concerns over the effect of inequality and the extreme fluctuations of the economy brought the Gilded Age to an end. The economy did not produce the change. Politics did.”

A couple of those “extreme fluctuations” were the railroad bubbles that burst in 1873 and 1893. The parallels between those bubbles and that of the current, supposed, AI one have been noted (for instance, here and here) and seem to me, clear. What replaced that Gilded Age was the Progressive Era, which shifted political and economic priorities and the definition of success away from sheer wealth accumulation towards addressing social issues like poverty and workers’ rights, and eventually the New Deal, which built the American regulatory state and social safety nets that the Trump administration is currently dismantling.9

It may take our current bubble bursting, and the subsequent economic pain, for our political economy to again change its definition of success.

As I’ve noted previously, this period was also one of intense globalization. Powered by the railroad and steamships, the expansion of the telegraph, and extractive colonialism, the world “shrunk” in size to the point where, in 1904, the father of geopolitics, Halfred Mackinder argued that the world was now in a closed political system.

I originally wrote “oligarchy” instead of “plutocracy” but there’s an important distinction here. While oligarchy simply means rule by few, plutocracy is a specific type of oligarchy in which wealth is the defining characteristic of power (via Claude).

That’s Gross Domestic Product or the total monetary value of all goods and services produced within a country's borders over a specific time period (via Claude).

At some point I’d like to do a deep dive on the concept of economic growth and how it is central to capitalism.

Claude assisted with the definitions in this paragraph.

This could mean investing elsewhere, as I noted, or it could mean simply saving their money and not investing it, which presents its own issues. In fact, the fact that capitalists are not finding enough opportunities to invest their capital and thus just accumulating it and creating a stagnation economic is a crisis Robinson addresses in his first chapter on “overaccumulation”.

A few notes here: 1) I just found a very interesting article the term neoliberal that I will hopefully get to next week. 2) Robinson also mentions a brief period in South America, specifically in Peronist Argentina where this was the case. I simply don’t know enough about that to truly cite it here. 3) It’s debatable how much of this was possible because of the opportunity for growth that the end of WWII provided. 4) There may be a way to embed the whole chart via HTML but I haven’t figured that out yet.

All the normal AI caveats should apply here. The underlying reports that Claude cites can be found here: Oxfam re: workers’ rights;

This is a story for another time.